In a new Deloitte survey of what measures Asia Pacific (APAC) companies are undertaking to manage costs and improve margins, Australian companies were found to have the least aggressive cost reduction targets in the region (74% of Australian respondents cited a cost reduction target of less than 10% and a further 18% cited no target) and despite this, 75 per cent are not meeting their cost reduction goals.

Deloitte’s biennial cost survey, Thriving in uncertainty: Cost improvement practices and trends in Asia Pacific, also found that Australian companies appear to be making an effort to reduce costs on many different fronts, citing all approaches to cost reduction more frequently than their APAC peers. The most widely cited tactic over the past 24 months was taking ‘targeted actions to reduce costs in a few divisions, business units, functions or geographies’ (87% of Australian respondents v 61% APAC average), followed by ‘drive all divisions, business units and corporate functions to reduce a fixed percent of their costs’ (71% v APAC average of 52%).

Vanessa Matthijssen, Deloitte strategy & transformation partner, said: “Australian companies take a more balanced approach to cost reduction and growth than our Asian counterparts, perhaps a reflection of our mature economy, political stability and a focus on strategic flexibility. Yet high failure rates suggest that cost reduction programs are not as effective as they could be, creating an opportunity for companies to significantly improve how they manage costs.

“The right approach for cost reduction varies from one company to the next, depending on its unique situation and challenges. However, achieving cost targets greater than 10% will generally require a cost management approach that is more strategic and transformational in nature, as tactical improvements alone are unlikely to produce more than single-digit cost savings.”

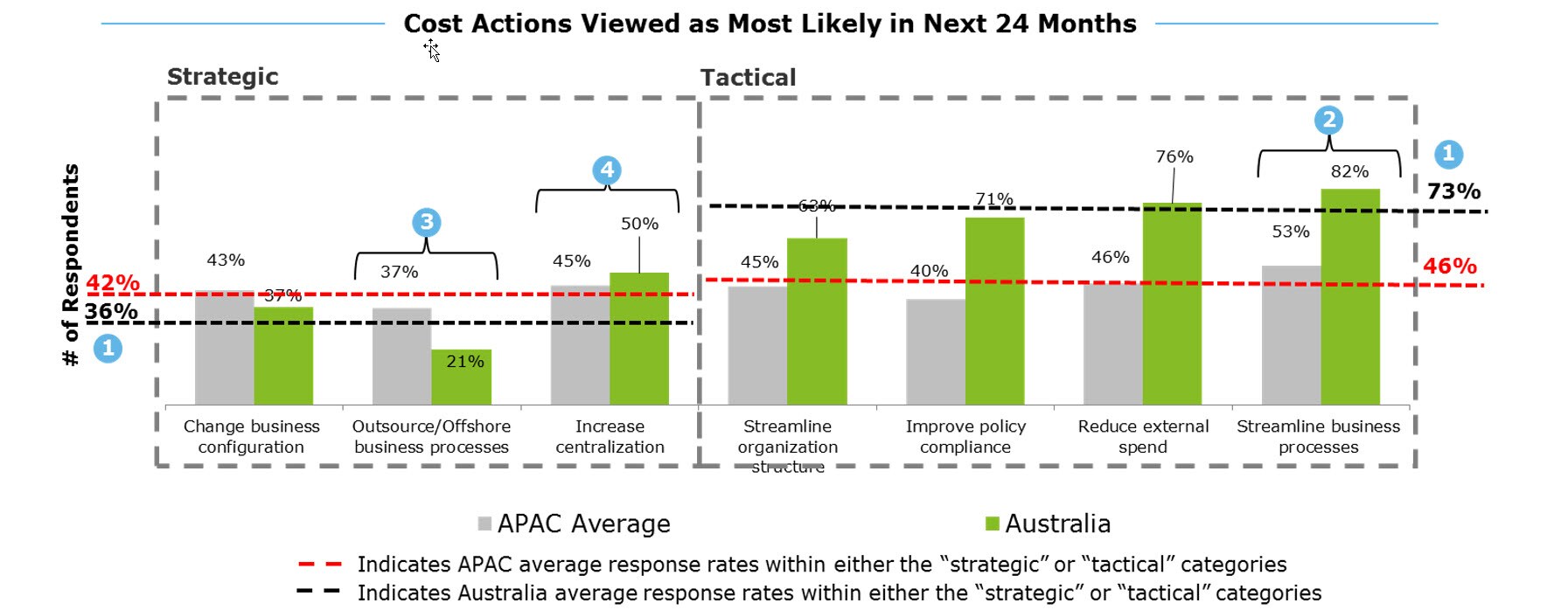

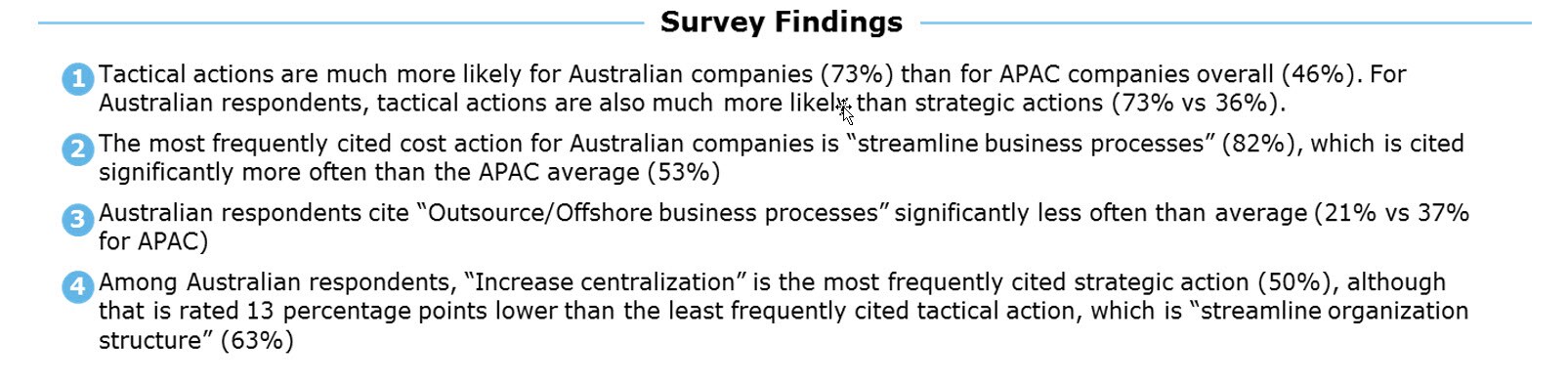

Looking to the future, Australian respondents predict that cost reduction initiatives in the next 24 months are likely to continue to be tactical rather than strategic in nature, with an average of 73% of respondents anticipating such actions as improving policy compliance (71%), reducing external spend (76%) and streamlining business processes (82%). The most frequently cited strategic action is to increase centralisation (50%).

“The relatively low expectations for taking strategic action on cost reduction initiatives may be explained by the fact that some Australian companies have already implemented significant actions, such as offshoring or outsourcing, and have shifted their attention to customer-centric growth transformations, which aim to deliver growth and cost efficiency simultaneously,” said Vanessa Matthijssen.

“However, to continue to retain competitive advantage, companies will need to adopt a more strategic and transformational approach to cost reduction, which is likely to include capitalising on digital breakthroughs such as robotic process automation (RPA) and cognitive technologies. They are changing the basis of competition and laying the groundwork for massive improvement in efficiency and effectiveness. Companies may soon find themselves needing cost improvements in excess of 50 percent, not just the 10 percent improvement that most are currently pursuing.”

The survey also found that Australian companies are less concerned about nearly all types of external risk than their APAC peers. In particular, two types of risk are noteworthy – political climate (5% of Australians rank as a risk vs 26% for APAC) and macroeconomic concerns (8% vs 25% for APAC) – because those risks are the top two ranking risks for APAC overall and particularly in China and Singapore.

Despite Australia’s comparative economic and political stability, looking ahead, Australian companies are slightly less optimistic than average about their future prospects for growth, although their overall outlook for growth is still decidedly positive (71% see annual revenue growth over the next 24 months, compared to 95% of Indian and 91% of Chinese companies and an APAC average of 78%).

APAC Insights

Across Asia Pacific, the top three strategic priorities are sales growth, product profitability, and cost reduction. India ranks sales growth the highest priority (73%) and India also cited balance sheet management much more frequently than the region overall (53% versus 20% for APAC).

Cost reduction programs are failing across APAC, not just in Australia. The majority of companies did not meet their cost reduction targets (range of 63% in China to 83% in India, with an APAC average of 72%). But Australia had the most conservative cost reduction targets by some measure (74% targeting less than 10% reductions, with the next closest country in that category being Japan with 50% and an APAC average of 43%). India has the highest targets for cost reduction, with 44% of Indian companies targeting cost reductions of more than 20%.

According to respondents, implementation challenges are the biggest barrier to effective cost management (61% in Australia, 60% APAC average). This is particularly true in India (73%) and China (72%) perhaps because they are pursuing the most aggressive cost targets.

The two most popular cost reduction approaches for respondents over the past 24 months were ‘intensifying existing productivity programs’ (62% average in APAC) and ‘targeted action to reduce costs’ (61% average, 87% in Australia). Zero-based budgeting (ZBB) is the least popular of the cost reduction approaches cited in the survey, although it is much more common in Australia (42%) than across the APAC region as a whole (20%).

The most frequently cited cost management capabilities developed over the past 24 months across APAC were: improved processes for forecasting, budgeting, and reporting (67% average, 87% in Australia); implement new policies and procedures (58% average v 76% in Australia); and set up IT infrastructure, IT systems, and business intelligence platforms (55% average v 63% in Australia).

About the survey

The Thriving in uncertainty report surveyed 299 business leaders (C-suite executives and senior management) from large and mid-size companies in Australia, China, India, Japan, Hong Kong and Singapore; comprising 89 per cent of the Asia-Pacific economy based on gross domestic product. The poll was conducted in January and February 2017.